Journal entries are recorded when an activity or event occursthat triggers the entry. Recall that an original source can be a formal documentsubstantiating a transaction, such as an invoice, purchase order,cancelled check, or employee time sheet. Not every transactionproduces an original source document that will alert the bookkeeperthat it is time to make an entry. Learn how to build, read, and use financial statements for your business so you can make more informed decisions. Not sure where to start or which accounting service fits your needs? Our team is ready to learn about your business and guide you to the right solution.

Accrued revenues

In December, you record it as prepaid rent expense, debited from an expense account. Then, come January, you want to record your rent expense for the month. You’ll move January’s portion of the prepaid rent from an asset to an expense. Adjusting entries are changes to journal entries you’ve already recorded. Specifically, they make sure that the numbers you have recorded match up to the correct accounting periods. This principle only applies to the accrual basis of accounting, however.

Accounting Services

To get started, though, check out our guide to small business depreciation. First, record the income on the books for January as deferred revenue. Then, in March, when you deliver your talk and actually earn the fee, move the money from deferred revenue to consulting revenue.

Accounting Adjustments

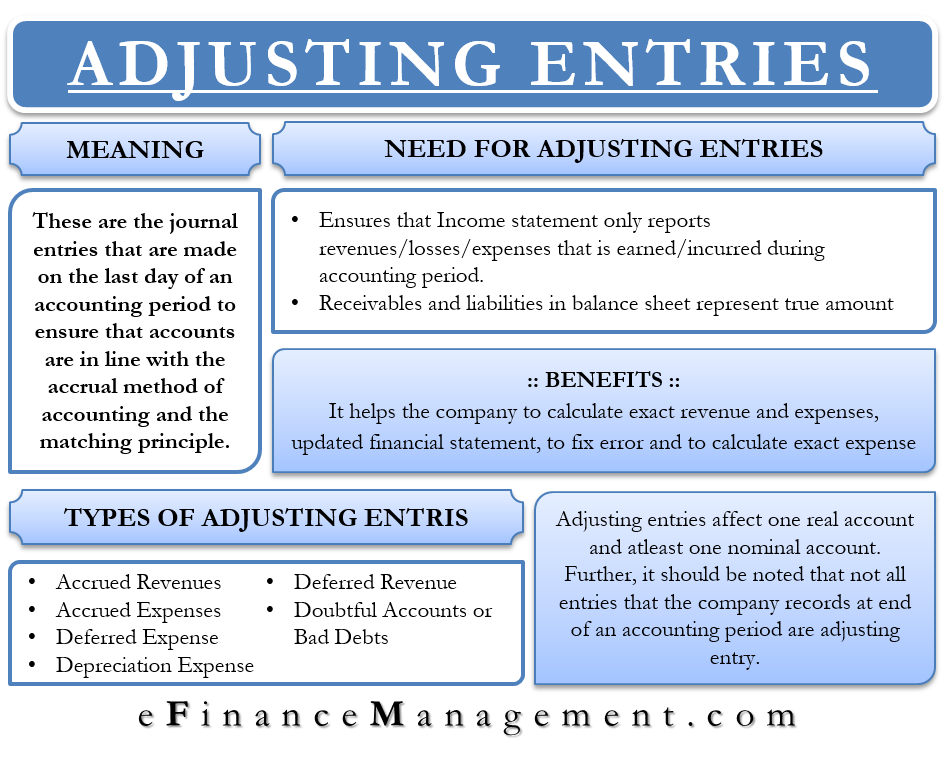

At the end of each accounting period, businesses need to make adjusting entries. The balance sheet reports the assets, liabilities, and owner’s (stockholders’) equity at a specific point in time, such as December 31. The balance sheet is also referred to as the Statement of Financial Position. As a result, there is little distinction between “adjusting entries” and “correcting entries” today. In the traditional sense, however, adjusting entries are those made at the end of the period to take up accruals, deferrals, prepayments, depreciation and allowances.

- At the end of the accounting period, you may not be reporting expenses that happen in the previous month.

- Each type of adjustment entry serves a specific purpose and is designed to ensure that financial statements are accurate and complete.

- After almost a decade of experience in public accounting, he created MyAccountingCourse.com to help people learn accounting & finance, pass the CPA exam, and start their career.

- Our team is ready to learn about your business and guide you to the right solution.

Such expenses are recorded by making an adjusting entry at the end of the accounting period. Using the tableprovided, for each entry write down the income statement accountand balance sheet account used in the adjusting entry in theappropriate column. Recall that unearned revenue represents a customer’s advancedpayment for a product or service that has yet to be provided by thecompany. Since the company has not yet provided the product orservice, it cannot recognize the customer’s payment as revenue.

As you move down the unadjusted trial balance, look for documentation to back up each line item. For instance, if you get to accounts receivable, you should have a list of all customers that owe you money, and it should exactly agree to the trial balance, which comes from the ledger. This account is a non-operating or “other” expense for the cost of borrowed money or other credit. The balance sheet reports information as of a date (a point in time).

All adjusting entries include at least a nominal account and a real account. For information pertaining to the registration status of 11 Financial, please contact the state securities regulators for those states in which 11 Financial maintains a registration filing. The primary objective of accounting is to provide information that will help management take better decisions and plan for the future.

After the first month, the company records an adjusting entryfor the rent used. The following entries show initial payment forfour months of rent and the adjusting entry for setting up payroll for small business one month’susage. Note that a common characteristic of every adjusting entry will involve at least one income statement account and at least one balance sheet account.

Leave A Reply (No comments So Far)

No comments yet