For this purpose, a business prepares “Final Accounts” (i.e., a Trading Account, Profit & Loss Account, and Balance Sheet). We prepare the Final Accounts straight away with the amounts stated in the Trial Balance.

Ask Any Financial Question

We at Deskera offer an intuitive, easy-to-use accounting software you can access from any device with an internet connection. We can break down steps five and six of the accounting cycle into a bit more detail. Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion for teaching.

Adjusting Journal Entries

To record deferred revenue, an adjusting entry is made to decrease the liability account and increase the corresponding revenue account. Accrued revenue is revenue that has been earned but not yet received. To record accrued revenue, an adjusting entry is made to increase the revenue account and increase the corresponding asset account.

Free Course: Understanding Financial Statements

Each one of these entries adjusts income or expenses to match the current period usage. This concept is based on the time period principle which states that accounting records and activities can be divided into separate time periods. The primary in a process costing system the number of wip inventories is to update account balances to conform with the accrual concept of accounting. Overall, adjustment entries play a crucial role in ensuring the accuracy and reliability of financial statements. Companies that take the time to properly record and adjust their accounts will be better equipped to make informed business decisions and meet their financial obligations. As an example, assume a construction company begins construction in one period but does not invoice the customer until the work is complete in six months.

- Using the tableprovided, for each entry write down the income statement accountand balance sheet account used in the adjusting entry in theappropriate column.

- Without adjustment entries, the financial statements would not be a reliable source of information for investors, creditors, and other stakeholders.

- A real account has a balance that is measured cumulatively, rather than from period to period.

- When the company collects this money from its clients,it will debit cash and credit unearned fees.

- At the end of hisfirst month, he reviews his records and realizes there are a fewinaccuracies on this unadjusted trial balance.

Another situation requiring an adjusting journal entry arises when an amount has already been recorded in the company’s accounting records, but the amount is for more than the current accounting period. To illustrate let’s assume that on December 1, 2023 the company paid its insurance agent $2,400 for insurance protection during the period of December 1, 2023 through May 31, 2024. The $2,400 transaction was recorded in the accounting records on December 1, but the amount represents six months of coverage and expense. By December 31, one month of the insurance coverage and cost have been used up or expired.

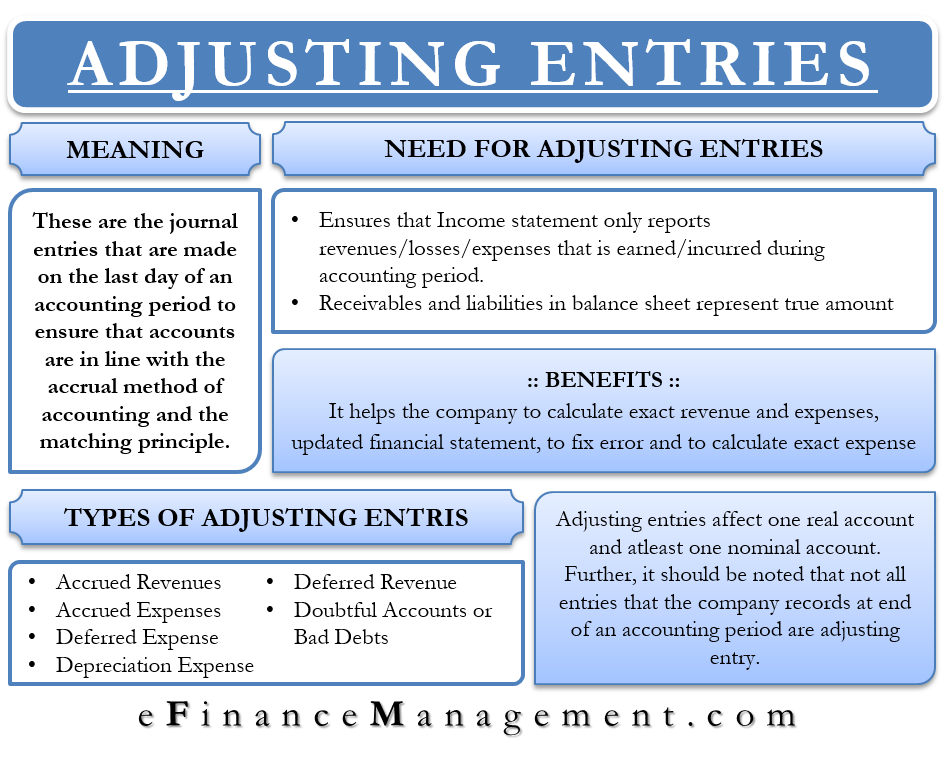

What Are the Types of Adjusting Journal Entries?

An adjusting journal entry involves an income statement account (revenue or expense) along with a balance sheet account (asset or liability). Periodic reporting and the matching principle may also periodically require adjusting entries. Remember, the matching principle indicates that expenses have to be matched with revenues as long as it is reasonable to do so. To follow this principle, adjusting journal entries are made at the end of an accounting period or any time financial statements are prepared so that we have matching revenues and expenses. According to the accrual concept of accounting, revenue is recognized in the period in which it is earned, and expenses are recognized in the period in which they are incurred.

Allowance for doubtful accounts is an estimate of the amount of accounts receivable that may not be collected. To record the allowance for doubtful accounts, an adjusting entry is made to increase the allowance for doubtful accounts expense account and decrease the corresponding asset account. Adjustment entries are an essential aspect of accounting that ensures financial statements are accurate and follow accounting principles. These entries are made at the end of an accounting period to adjust accounts and reflect any changes that have occurred during the period. Deferrals refer to revenues and expenses that have been received or paid in advance, respectively, and have been recorded, but have not yet been earned or used. Unearned revenue, for instance, accounts for money received for goods not yet delivered.

This means that the bookkeeper or accountant must ensure that all adjustment entries are made before financial statements are prepared. In the income statement, adjustment entries are used to update the values of revenue and expenses. For example, if a company has recognized revenue that has not yet been earned, an adjustment entry is made to remove this revenue from the income statement. Similarly, if a company has incurred an expense that has not yet been recognized, an adjustment entry is made to include this expense in the income statement. To record a prepaid expense, an accountant would debit an asset account and credit a liability account. Accruals are types of adjusting entries thataccumulate during a period, where amounts were previouslyunrecorded.

Atthe end of a period, the company will review the account to see ifany of the unearned revenue has been earned. If so, this amountwill be recorded as revenue in the current period. Booking adjusting journal entries requires a thorough understanding of financial accounting. If the person who maintains your finances only has a basic understanding of bookkeeping, it’s possible that this person isn’t recording adjusting entries.

Leave A Reply (No comments So Far)

No comments yet